Aadhaar eSign Mandate & API Mandate – A Comparison

Established by the RBI and the National Payments Corporation of India, emandate is a digital payment solution to help businesses simplify their payments. This procedure is built on an underlying NACH (National Automated Clearing House) infrastructure, for businesses to collect payments without the need for manual involvement. It can be broadly divided into three parts – physical mandate, Aadhar-based esign mandate, and API mandate.

To elaborate on eNACH’s meaning, Electronic National Automated Clearing House or can be described as an upgrade over the traditional NACH because it enables the process of payments easier and time friendly. eNACH emandate enables high-volume, low-value electronic transactions between banks that are periodic and recurring online.

eMandates play a crucial role in easing the management of recurring payments such as a loan or purchase EMIs, premiums for health & life insurance policies, and other monthly payments for subscriptions or donations to different sectors like NGOs. This reduces friction in payment collection by streamlining payment reminders and minimizing late charges for the customer. In a nutshell, e-mandate benefits both the customers and the organizations involved.

The Mandate Process

Majority of the banks and other institutions maintain the following process when it comes to issuing mandates manually:

-

- A signed form is collected from the customer which exhibits the fact that he/she has given consent to the bank to debit a specific amount money in a recurring manner automatically from the existing bank account (Destination bank).

- The bank forwards this form to the NPCI where a UMRN or Unique Mandate Reference is created. The form is then sent back to the destination bank where the customer has his/her account.

- Upon the acceptance of the form by the bank, the process of auto-debit is initiated.

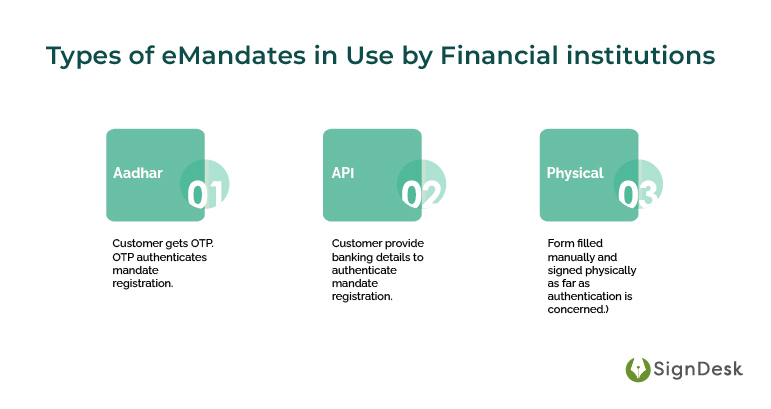

Types of eMandates in Use by Financial institutions

Apart from making payments easy, e-Mandate also serves a lot of purposes. The types of e-Mandate that prevail are as follows:

- Aadhaar-based mandate

In an aadhaar esign-based mandate, the customers receive a One Time Password (OTP) in their registered mobile number. The OTP is entered into the portal of the eNACH eMandate service provider to authenticate the mandate and carry out the mandate registration process.

- API mandate

In this variant, an Application-Programming Interface (API) will be created with the help of an integrator, enabling businesses to source the data that they require about the customer. In an API-based mandate or enach API mandate, customers must authenticate the mandate using their Netbanking or debit card details for the e-mandate API.

- Physical mandate

Physical mandate is the oldest form of a mandate that are filled manually and is authenticated by the payer who signs physically. This is usually a time-intensive process where the mandate paperwork goes through numerous stages and organizations.

What is an API mandate?

An application-programming interface (API) is a collection of programming instructions and standards for gaining access to a Web-based software application or Web utility that enables two apps to communicate with one another. It is a simple way to get through one’s exclusive instrument via an evolution of cloud-native applications. It also helps to distribute data with the users who are not part of the domain and other customers.

In this case, an API mandate means that organizations leverage an API for their payments portal with help from an API eMandate service provider. This eMandate API will allow businesses to capture any mandate-related information. Moreover, the business site connects the consumer to the bank page via the NPCI interface for verification selection and mandate authentication using either internet banking credentials or debit card credentials.

The NPCI also states that the customer must ensure that all of the mandate data he or she is about to validate via eMandate APIs are authentic. After providing consent in this regard, the customer has to opt for the authentication mechanism and authorize the mandate using his/her information.

The steps involved in the API mandate are as follows:

- The data is collected by Signdesk’s portal and shared with the NPCI – ONMAGS page

- The customer consents to share their mandate details on this page.

- The data is then loaded and the customer is redirected to the destination bank.

- The customer enters their Netbanking or debit card details here for validation.

- From the destination bank, the mandate information is submitted to NPCI and the mandate is registered.

- A UMRN number is generated for this mandate for tracking purposes.

This is how an API e-mandate is carried out.

Aadhaar eSign mandate – Meaning & Applications

The eSign electronic signature service is a cutting-edge project that allows for the simple, efficient, and safe signing of electronic documents by authenticating signers utilizing Aadhaar eKYC services.

Initiated by NPCI, or National Payments Corporation of India, a division initiated by the Reserve Bank of India whose aim is to operate retail banking and orders of settlement in India, the Aadhaar Payment Bridge or APB System has enhanced the Direct Benefit Transfer (DBT) scheme of the Government and Government Agencies and turned it into an achievement.

It helps in streamlining the benefits and schemes initiated by the government through the Aadhaar numbers. Also, it acts as a bridge between Government and the banks that sponsor them with the beneficiary and their banks.

eSign mandate undergo the following steps:

- Customers are invited to log into SignDesk, where mandate details are entered.

- The customer consents to their Aadhaar details being shared with the corporate client.

- An OTP to the linked mobile number is shared and the same needs to be entered in the portal.

- If the OTP matches, the authorization is approved by NsDL and the validated data is sent to SignDesk. If rejected by NsDL, the process is re-initiated.

- SignDesk then shares the data with the sponsor bank who in turn shares it with NPCI

- NPCI then shares the same with the respective destination banks.

- The confirmation from the destination banks are sent back to NPCI and NPCI then shares the response to the Sponsor bank

- The response from NPCI is shared with SignDesk & the destination banks, which debits the required funds.

The Supreme Court had ordered the NPCI to discontinue the Aadhaar-based service on November 23, 2018, but eSign mandates have recently been legitimized and are emerging as one of the popular ways of setting up emandates.

API mandate or Aadhaar eSign mandate: Which One to Choose?

As explained above, both API mandate and Aadhaar based eSign mandate ease out the process of eNACH or mandate when compared to the physical mandate which are done manually.

Between the API mandate and the Aadhaar based eSign Mandate, the API-based emandate require the customer to provide their net banking or debit card details to carry out the process, which has the chances of getting affected by cyber attacks. This further can lead to fraudulent activities and deception.

In the case of the eSign mandate, the user just has to put the OTP that they receive on their phone number which is linked to their Aadhaar card. This generally takes 3-5 days compared to the real-time delivery of API mandate but involves near to no risk when it comes to safety.

However, both Aadhaar & API mandates provide FIs provisions to upload mandate orders in bulk, something that banks can’t accomplish with physical mandates.

Here are the key differences financial institutions need to know regarding API mandates vs Aadhaar eSign mandates.

|

API eMandate |

Aadhaar eSign eMandate |

|

|

How to validate |

Netbanking or debit card |

OTP-based Aadhaar eSign |

|

How long to register |

Real-time registration |

2 days |

|

Available in how many banks |

45+ banks |

40+ banks |

|

Success rate |

95% |

80% |

|

IFSC/MICR |

No |

Yes |

In June 2020, in a circular by NPCI it was ordered that the customers will be able to validate their esign mandate using Aadhaar-based eSign, which will increase efficiency and the speed with which banks can now handle mandate. It was suspended by Supreme Court due to Aadhaar-related issues in November 2018.

Following the Supreme Court’s decision to suspend the eSign-based techniques, the NPCI established the API mandate solution, as an alternative route remotely verify consumers. While successful, none of these had the reach that Aadhaar- and OTP-based permission did.

eSign mandates have recently been permitted again by NPCI, albeit requiring more validations than the previous Aadhaar-based eMandate procedure.

SignDesk’s Link.It: eMandate Solution for smooth recurring payments

Link.It by SignDesk offers an NPCI-compliant eNACH eMandate solution to easily automate recurring payments. Our system manages recurring payments by permitting the customer’s bank to debit the account on a regular basis. SignDesk’s e-Mandate solution also enables clients to easily validate e-mandate whether its Aadhaar based eSign mandate, or API mandates like NetBanking, or debit/credit card credentials, as well as set up regular auto-debit transactions for your company.

Several big banks and financial institutions utilize SignDesk’s eMandate and eSign technologies to save costs by 60-85 percent and reduce turnaround time by more than 50 percent.

Customers may utilize Aadhaar-based authentication to digitally sign documents using eSign processes, and our NPCI-compliant E-Mandate solution enables quick and easy payment collection for bills, subscriptions, contributions, and loan EMI payments.