AML Insurance- Insurance Industry & Money Laundering

Money laundering and fraud in the insurance sector costs businesses and customers anywhere between 40 billion and 300 billion dollars per year. This high risk of financial crime makes it imperative for insurers to adopt AML guidelines and due diligence best practices to combat money laundering and other illicit activities.

There are numerous opportunities for money laundering in the insurance industry. Criminals are increasingly exploiting insurance products & services to legalize black money & commit fraudulent activity.

Insurers are an easier target because fewer counter-measures exist in the industry. Thus money launderers exploit insurance products to ‘clean’ the funds they accumulated through illicit activities like corruption, drug trafficking, major thefts, & other such crimes.

Leveraging secure digital KYC solutions with AML screening integrations, helps insurers get a leg up on criminals and bad actors looking to exploit insurers to conceal ill-gotten funds.

How Do Criminals Exploit Insurance Products? – AML Risks In Insurance

Criminals use the insurance industry to legitimize their illicit gains in several ways. Listed below are some examples of insurance products that are usually of interest to money launderers & terrorist financiers. Insurance products vulnerable to money laundering include:

- Annuity Policies: High regular premium savings products like annuity policies serve as vehicles for money laundering. Criminals purchase the product & pay premiums using fraudulent funds. Once they start receiving income from the insurance contract, they can earn legitimate money.

- Policy Ownership Transfer: Another tool money launderers use in the insurance industry is transferring policy ownership. Here, the customer purchases an insurance policy whose ownership he moves to a criminal third party, i.e., the money launderer. The criminal will then be able to withdraw ‘clean’ money.

- Single Premium Policies: Single premium insurance presents yet another opportunity for money laundering. They allow criminals to discharge large amounts of money in one transaction. Criminals use their unlawful funds to purchase a single-premium insurance policy, then attempt to recoup it by filing fraudulent claims.

- Top-Ups: Top-ups are another means criminals use to legitimize their illicit funds. They pay a small amount of initial premium so as to avoid attracting regulatory attention. After that, they deposit more illicit funds through top-ups to offload more illegal money.

- Cooling-Off Periods: Money launderers can claim a refund for premiums they paid during the cooling-off period, overpay premiums intentionally or surrender their policies at a loss to receive a refund.

- Policy Loans: Criminals can use their life insurance policy’s cash value as collateral for loans after increasing its value through premium payments.

Why Is It Important To Prevent Money Laundering?

It is highly critical that insurance provider companies prevent any possibility of money laundering in transactions that take place regularly. Putting a stop to money laundering helps:

- To preserve the company’s reputation & increase customer trust

- To safeguard the company, since organized crime disrupts established business practices

- Take reasonable steps & exercise due diligence to prevent the use of the company as a vehicle for money laundering.

Criminal money is used to finance further criminal activity, increasing unlawful pursuits. And the implication of money laundering, including AML crypto, is equivalent to abetting/participating in the criminal act itself. Hence it is essential that insurers pre-empt any instance of money laundering.

AML compliance in insurance focuses on anti-money laundering procedures that deter and prevent potential offenders from engaging in money laundering fraud or crime. Criminals cannot conceal the illicit origin of money in any type of transaction in this manner.

For this reason, insurance companies must establish strong AML compliance practices & prevent money laundering in the industry.

How Can Insurance Providers Spot Money Laundering? – AML Guidelines For Insurance Companies

As mentioned above, perpetrators have multiple avenues to launder money through the insurance industry. For this reason, insurance companies must prioritize compliance with AML insurance-specific regulations & implement proper procedures to prevent these activities.

The IRDAI subjects insurance firms to various anti-money laundering regulations to help them prevent opening routes for the misuse of insurance products & funds. They enable insurers to spot money laundering activities & help avoid them early on.

The methods to identify & prevent money laundering in the insurance sector include knowing the customer, screening for sanctions, monitoring transactions & appropriate supervision.

- Knowing Your Customer- KYC

Given the potential risk of money launderers using insurance services, insurers should make every effort to determine the true identity of their customer.

The AML requirements for insurance companies necessitate that they implement a robust KYC or Know Your Customer process before onboarding customers. Insurance companies must implement KYC procedures to identify the individuals with whom they intend to do business and analyze the vulnerability that comes with working with them.

Insurers must identify individuals & entities that buy insurance from them. To conduct KYC procedures, insurance companies must collect personal information to verify an individual’s or business’s identity. They have to verify that the collected information holds & the customer is risk-free.

- Sanctions Screening

It is a type of AML measure in which insurers must ensure that a potential customer does not appear on a list of individuals or entities prohibited from purchasing certain life insurance products.

- Transaction Monitoring

Insurance companies must monitor their customers’ transactions that deal with permanent life insurance policies, annuity contracts, & any other insurance product with cash value or investment features.

They must impose a risk-based insurance transaction monitoring process to identify money laundering risk levels & mitigate them using suitable measures.

Insurance providers must monitor their customers’ policy loans, surrenders, cancellations, & withdrawal requests. Additionally, they should also keep an eye out for changes in payment methods and unusual/suspicious loan repayment activity, as well as the rate of refund premiums, surrenders, redemptions, & withdrawals.

- Adequate Supervision

Ample supervision is required within the insurance company to ensure that all AML insurance measures are properly implemented and enforced.

As per the IRDAI regulations, insurers should appoint or assign a Designated Director to ensure overall compliance with the obligations imposed by the PML Act & Rules. A Senior Principal Officer (PO) has to be appointed to ensure compliance with the PML obligations.

The compliance officers must ensure that AML risks are managed & monitored & that all insurance activities are carried out in accordance with regulations.

- Due Diligence

The AML requirements for insurance companies require insurers to take a risk-based approach to identify & deter money laundering activities successfully. To achieve this, they must establish a customer or client due diligence process which verifies customers & categorize them as per the risk they pose.

Insurers can classify their customers based on parameters such as their identity, nature of the business activity, business location, social or financial status, etc.

- Low-Risk Customers: Individuals and entities whose identities & sources of wealth can be identified, & transactions whose policies generally conform to the known profile are classified as low risk. These customers require simple due diligence.

- High-Risk Customers: Non-resident customers, companies with close family shareholding or beneficial ownership, firms with sleeping partners, trusts, charities, NGOs, & organizations receiving donations, politically exposed persons (PEPs), and those with a questionable reputation based on publicly available information are classified as high risk. They need to be under higher due diligence.

Types Of Due Diligence For Insurance Customers:

- Simplified Due Diligence: In the case of individual policies where the aggregate insurance premium is less than Rs 10000/- per annum, insurers can use simplified due diligence measures. It is a less stringent customer verification process that requires only basic information like the customer’s name, address, and a valid form of identification.

- Enhanced Due Diligence: Insurers should investigate all complex, unusual patterns of transactions with no evident economic or legal purpose to implement enhanced due diligence. Insurers must assess the client’s ownership and financial position, including the source of funds, concerning the identified risks & product profile.

- Ongoing Due Diligence: Any change inconsistent with the customer’s normal & expected activity necessitates additional continuous due diligence processes & action. In addition to verifying the customer’s identity during insurance issuance, insurers must conduct ongoing due diligence & risk assessments whenever a customer makes supplemental financial transactions.

How Does VBIP-Powered KYC Aid AML & Compliance In Insurance Companies?

Given the high risk of money laundering in the insurance sector, companies in this industry need to take all necessary measures to guarantee that they do not provide criminals with a means to launder their illicit funds.

KYC powered with VBIP or video-based identification process acts as an effective method with which insurers can establish their customer’s authenticity. VBIP assists insurers & insurance customers complete KYC more efficiently & often with fewer drop-offs.

VBIP enables insurance providers to conduct KYC & customer screening procedures remotely, helping them categorize their customers’ risk profiles faster.

Following a few simple steps, insurance providers can seamlessly conduct video-based identification for their customers on secure AI-powered video KYC platforms like SignDesk.

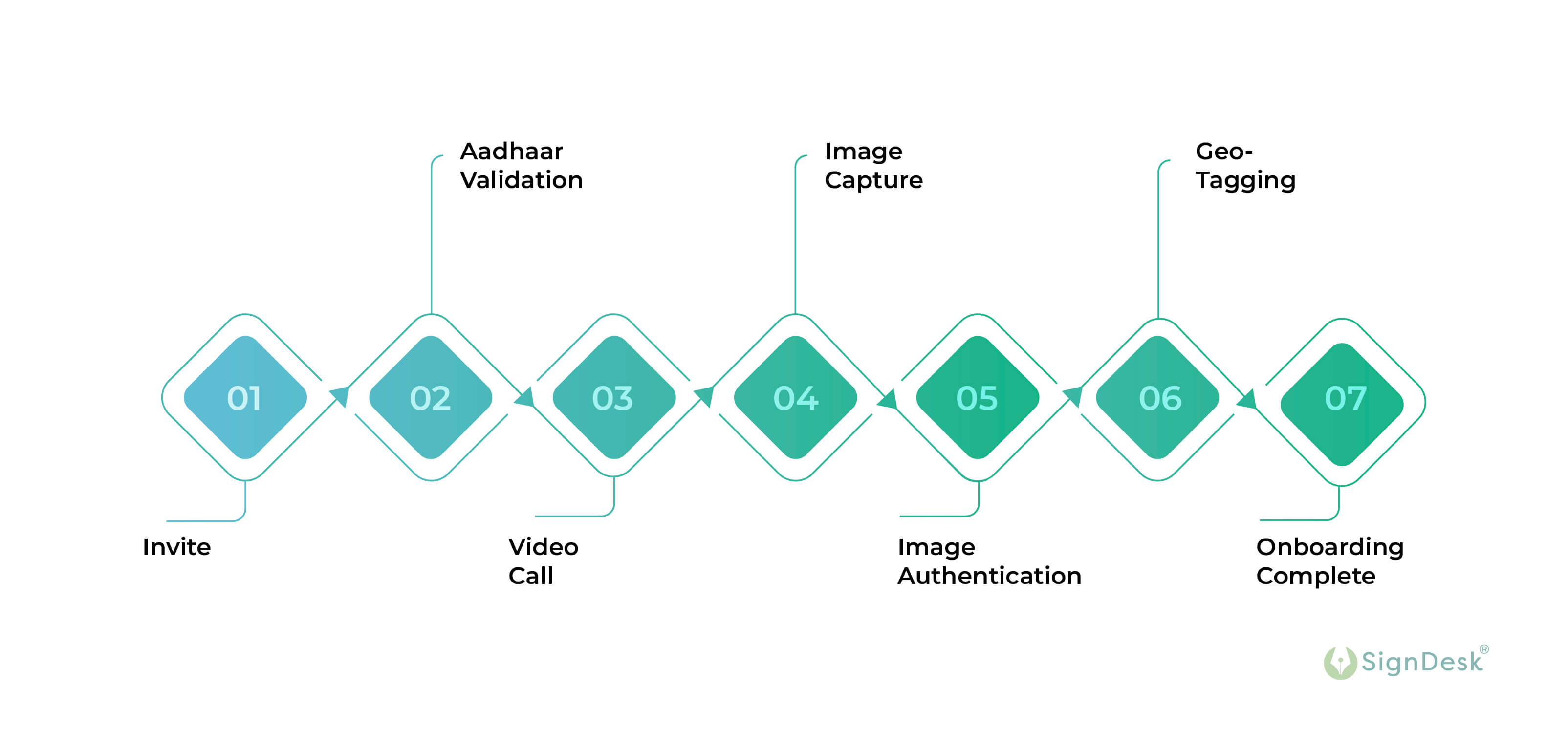

VBIP- How Does Video-Based Customer Verification Take Place?

Insurance Customer Verification With VBIP

- Step 1: Request the customer’s consent to the VBIP & initiate video KYC.

- Step 2: The customer’s Aadhaar is validated, or the customer uploads & validates OVDs with Aadhaar eSign.

- Step 3: An authorized insurance representative initiates an audio-visual interaction with the customer & records the video.

- Step 4: The customer’s live photograph & document images are captured.

- Step 5: Machine Learning techniques are used to match the customer’s photo with the photos on their IDs.

- Step 6: Using AI and OCR technologies, visual data is extracted & validated against a standard database.

- Step 7: Geo-tagging is used to determine the location of the customer.

- Step 8: The video-based identification process successfully verifies the customer.

SignDesk: AI-Powered VBIP Platform For Insurers

KYC, including ekyc for insurance is essential in preventing money laundering, & insurers must establish a robust customer verification system to spot money laundering & comply with the AML insurance sector regulations.

SignDesk‘s innovative VBIP solution is designed specifically for this purpose, & it provides insurers with a reliable video-based customer identification & verification solution. Insurance firms can efficiently conduct remote customer verification with increased accuracy to detect & put an end to money laundering.

Schedule a demo with our KYC experts today to learn about & implement VBIP for your customers.