KYC Verification & Blockchain Technology – Overview & Challenges

KYC verification is the straightforward process of authenticating a client, employee, vendor, or stakeholder’s identity using validating factors. These factors could include photo-based IDs, facial features, answers to randomized questions, etc which gets easier via blockchain KYC.

For a KYC verification process to be considered successful and valid, the factors mentioned above must be validated according to rules prescribed by regulatory bodies.

KYC verification is necessary across several sectors, including finance, banking, securities, insurance, and more. This means that businesses, including banks, insurers, investment firms, and NBFCs conduct tens of thousands of KYC verification transactions every day.

Due to the sheer volume of daily verification transactions, the traditional sequential approach wherein individual verification queries are validated to a high degree of confidence.

Once the relevant authorities verify identities, KYC verification is completed.

Clearly, such a system will have problems scaling to keep up with business growth. Other challenges include an over-reliance on centralized authorities for authentication, the possibilities of errors and a lack of fail-safe mechanisms, and a noticeable lack of efficiency.

Blockchain-based KYC verification offers an excellent alternative to standard methods of KYC verification. This is because DLT enables businesses to gather information from many service providers into one cryptographically secure and unchanging database using emerging techniques from decentralized blockchains.

This eliminates the requirement for a third party to validate the veracity of the knowledge.

In fact, the ability of blockchain technology to independently and efficiently verify knowledge is among the most significant advantages of leveraging DLT for customer verification.

Blockchain is among the technologies thought to hold the key to eliminating inefficiencies and duplication in KYC processes.

What is a Blockchain KYC process?

For Distributed Ledger Technology, the process of using Blockchain for KYC goes through several stages.

Below is an example of blockchain KYC verification involving two Financial Institutions (FIs). In a hypothetical situation, the first FI (FI-1) conducts KYC verification for a client, and the second FI (FI-2) must then conduct the same KYC transaction.

For a standard KYC system, this would involve conducting KYC verification for a second time. For a blockchain KYC system, the process will go quite differently.

Let’s walk through the steps of KYC verification using blockchain:

- Profile Creation:

FI-1 conducts KYC verification on a blockchain-based KYC platform, which the user configures using their identity documents. Once uploaded, the data is available to FI-1 for verification.

When it comes to storing user data, there are now several options for FI-1:

- On a centralized, secure server

- On FI-1’s private Server

- On the blockchain

If FI-1 is using a blockchain-based KYC verification platform, user data is stored on a shared blockchain.

- Transactions with FI-1:

When a user conducts a transaction with FI-1, they grant FI-1 access to the user’s profile. FI-1 then validates the KYC data and saves a copy on their server. Following this, the respective hash is uploaded to the DLT platform.

Finally, FI-1 uploads digital copies of KYC details to the user’s profile, which is embedded with a hash function that corresponds to the hash function uploaded on the DLT platform.

- Transactions with FI-2:

When FI-2 requests KYC from the user, the user grants FI-2 access to their user profile. The KYC data (and its hash function) is then compared to the hash function uploaded by FI-1. If the two match, FI-2 will know that the KYC information received is valid as the verification details are the same as those of FI-1.

If the hash functions do not match, FI-2 must manually validate the customer’s KYC documents.

Here, as opposed to the traditional digital KYC process, the second FI was not required to conduct its own KYC verification for the customer. Instead, the two FIs simply refer to the immutable information on the blockchain to conclude the customer’s second KYC transaction.

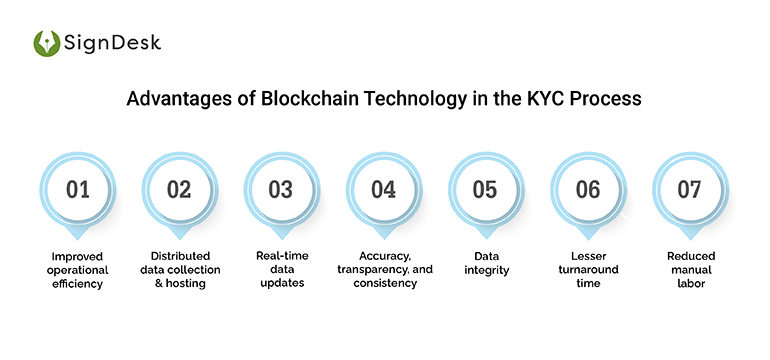

Advantages of Blockchain Technology in the KYC Process:

According to a report from 2016, 23% of financial firms want to adopt blockchain for securities cleansing and settlement.

Utilizing decentralized technology in KYC is more than just a simple fintech offering. Blockchain-powered KYC verification has enormous potential to boost transparency, collaboration, and efficiency for businesses functioning in regulated sectors.

- Improved operational efficiency

Scalable digital processes and secure user information sharing on a permissioned network can significantly reduce the effort and time required in the early stages of KYC. This also shortens the customer onboarding process and reduces regulatory and compliance costs.

- Distributed data collection & hosting

The use of blockchain technology in KYC puts data on a decentralized system that can be retrieved by only those parties who have been granted permission. Furthermore, the system provides adequate data security because data can only be accessed after users grant permission, eliminating instances of unauthorized access.

- Real-time data updates

When an FI completes a KYC transaction, the data is shared on a distributed ledger. This Blockchain technology KYC system allows other participating institutions to access real-time updated information with the assurance that they will be notified if there is a new addition or modification to the documents.

- Accuracy, transparency, and consistency

KYC Blockchain systems enable transparency and immutability, allowing FIs to validate both the data and the trustworthiness of data on the DLT platform. The decentralized KYC process streamlines the process of gaining secure and timely access to updated user data. This reduces the time and effort required by an institution to gather information.

The following are some of the additional advantages of using a Blockchain solution for KYC:

- Data Integrity: All data changes are tracked and monitored in real-time.

- Lesser Turnaround Time: FIs gain direct access to data through KYC Blockchain software solutions, reducing data gathering and processing time.

- Reduced Manual Labor: KYC on Blockchain eliminates the need for paperwork.

The Risks Involved in Blockchain-Based KYC

The process of blockchain-based KYC has enormous benefits in terms of protecting financial services and ensuring the legitimacy of the economies. However, the labor and resource-intensive nature of blockchain KYC make it a thorny issue for institutions worldwide.

- Anti-compliance risks:

Companies that fail to comply with KYC regulations face significant risks. Global institutions were fined $10.4 billion in 2020 alone for anti-money laundering (AML), KYC, and data privacy violations. This appears enormous, but untangling the complex and relentless requirements makes clear how many regulatory hoops institutions must jump through.

- Continuous & ongoing verification regimes:

KYC verification is not a one-time transaction where FIs verify an individual’s identity and continue to provide services with no other verification checks. In fact, institutions must conduct ongoing checks and monitor customer transactions, which consumes significant time and resources.

Blockchain-based KYC, due to the resource-intensive nature of the cryptographic transactions that are carried out, might not be the best option for continuous KYC verification.

- Maintaining regulatory compliance for cross-border transactions:

Institutions must also ensure that all applicable regulations are followed, which can be difficult when facilitating transactions across borders and regulatory zones. When one considers the various regulations in place worldwide, which are frequently filtered through larger legislative nets (GDPR and MiFID II, to name a few), the vast array of compliance processes becomes apparent. Maintaining compliance with these varying regulatory regimes is a challenge when using blockchain technology for KYC.

Blockchain-Based Verification: Decentralized & Efficient Verification

In the KYC verification process, gathering and processing information not only takes a significant amount of money, time, and effort but also leaves very few resources available for monitoring and analyzing user transactions and accounts for abnormalities.

Blockchain technology in KYC can reduce the time required for arduous processes by providing quick access to up-to-date data, which can then be used to solve more difficult KYC challenges.

However, blockchain will not be able to fix all of the challenges businesses are likely to face when undertaking KYC verification. Financial organizations will still have to continuously validate user KYC data once acquired, and extensive compliance regimes will still have to be complied with.

However, when it comes to increasing efficiency and data security, businesses would do well to fully leverage emerging technologies such as DLT.

On-chain KYC for blockchains, the first of its type, may be used to assess a variety of criteria, allowing individuals to fully interact with blockchain solutions while remaining compliant.

KYC verification is becoming increasingly crucial for FIs and regulated businesses in general, due to a pronounced increase in cyber-attacks following trends of widespread digitization. As these trends show no sign of letting up, FIs will have to be more proactive in leveraging decentralized technologies to make KYC verification safer and faster.

SignDesk’s KYC Solution for Verification

Signdesk’s cutting-edge compliance technology-based verification solution, ‘scan.it has helped 400+ clients minimize onboarding costs, reduce KYC drop-offs, reduce TAT by more than 50 percent, and protect against fraud.

Having been awarded the Best AI/ML Product at InnTech 2020 and the Best Digital Onboarding Product of 2020 from the Global Banking & Finance Review, our AI-powered digital onboarding solution offers real-time ID verification, facial matching or face verification, and customizable KYC workflows for banks and NBFCs to verify customer KYC securely and instantly.

Are you ready to join 400+ enterprises using Video KYC to verify and onboard customers? To get started, schedule a free demo with us now and experience the numerous Video KYC benefits.