PFRDA allows Video KYC

PFRDA (Pension Fund Regulatory & Development Authority) has been one of the most proactive regulatory bodies in the adoption of digital methods.

The organization has permitted OTP and eSign-based Aadhaar authentication for opening NPS (National Pension System) accounts, offline Aadhaar authentication using XML files or QR codes, e-exist and e-nomination for NPS accounts, and paperless onboarding, to name a few.

However, NPS subscribers still had to be physically present at certain Points of Presence (PoPs) or nodal offices for In-Person Verification, to avail a handful of NPS services.

With the recent envisage of a Video-based Identification Process (V-CIP) for onboarding, exit, or any other services related to NPS, pensioners can expect a completely digital experience and handle their NPS accounts with ease.

The adoption of V-CIP will massively benefit the PoPs serving as intermediaries between NPS subscribers and the NPS architecture by reducing the burden of documentation and streamlining NPS services. These PoPs include several major banks, NBFCs, and publicly owned companies such as Reliance Capital Ltd, HDFC Securities Ltd, Kotak Mahindra Bank, Axis Bank, Yes Bank, ICICI Securities Ltd, Bajaj Capital Ltd, SBI, SHCIL, and so forth. Paytm Payments Bank Ltd was also recently granted permission to act as a PoP for NPS services.

So how can these PoPs conduct V-CIP?

What do the PFRDA V-CIP guidelines say?

V-CIP is a video-based process for verifying the KYC of a customer and onboarding them remotely. V-CIP consists of – verifying KYC documents online, audio-visual interaction to ensure liveness, face match for identification, and geo-tagging.

The press release announcing V-CIP distinguishes two types of V-CIP – one procedure for mobile application-based VCIP and another for non-mobile applications.

Here are the basic rules and features of V-CIP for both mobile and non-mobile applications.

V-CIP for mobile applications

- The application must only be used by an authorized official of the PoP

- PoPs must ensure that the application is seamless, real-time, secured & end-to-end encrypted. The quality of the video must be sufficient to establish the customer’s identity beyond any doubt.

- The customer must upload their photo/signature and OVDs (Officially Valid Documents) via DigiLocker

- Documents can also be uploaded by scanning them live on the application

- There must be a random action initiation, usually in the form of an audio-visual interaction comprising of random questions and answers, to ensure that the video is not pre-recorded

- A live photo and live signature of the customer must be captured to match them with the photo and signature on the OVDs

- The customer’s location must be determined using geo-tagging

- The customer’s bank account must be verified through penny-drop mechanism

- A liveness check is to be carried out to safeguard against fraud

- The recorded video must be stored safely with timestamps, date and GPS coordinates

V-CIP for non-mobile applications

- The customer’s consent must be obtained before beginning V-CIP

- V-CIP is to be conducted by a trained and authorized official from PoP.

- A photo and the signature of the customer must be uploaded

- The customer must be display the specified OVD during V-CIP so that the details and photo can be captured

- A live picture of the customer is captured and matched with the photo on their documents

- The official must make sure that the video is clear and conduct an audio-visual interaction with the customer consisting of a randomized sequence of questions to ensure that the interaction is not pre-recorded

- The customer’s bank account is verified through penny-drop mechanism

- The recorded video must be stored along with timestamps, date, activity log, and the credentials of the authorized official

It must be noted here that V-CIP must be triggered from the domain of the PoP and not from a third party.

These two procedures are not vastly different and have a large portion of steps in common. So what will V-CIP for NPS look like in practice?

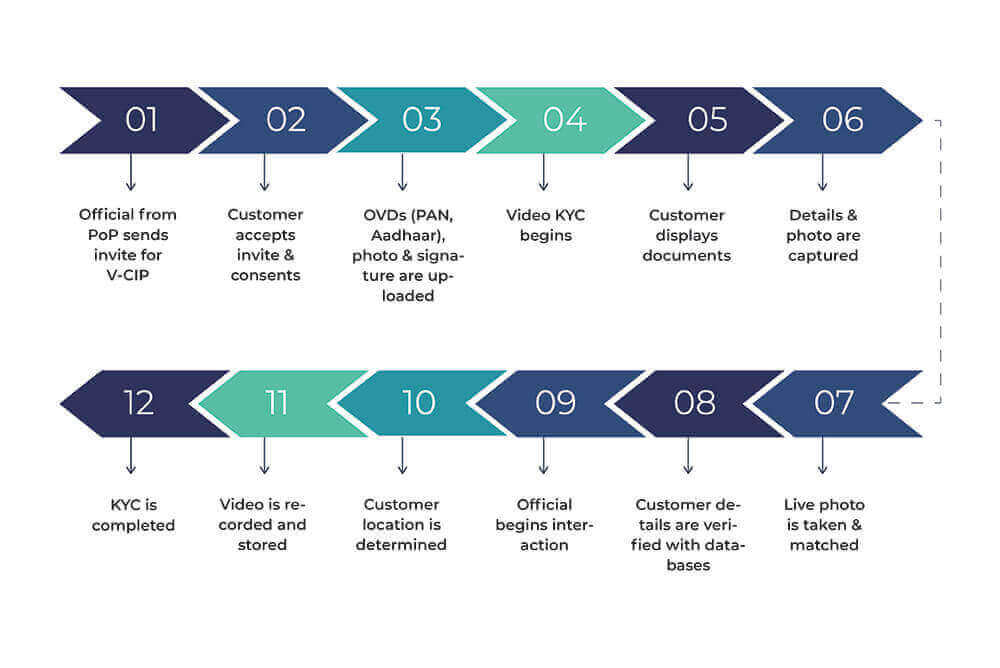

How V-CIP will look when implemented

The two procedures envisaged by PFRDA can be condensed to create a common workflow for both mobile and non-mobile V-CIP. Here’s how it will go with SignDesk’s AI-powered video KYC solution.

Award-winning Video KYC

SignDesk uses AI & ML to create a seamless and secure digital onboarding solution that is in use by several major banks, and has been awarded the Global Banking & Finance Review’s Best Digital Onboarding Product in India for 2020.

We use cutting edge facial matching technology and OCR-based data extraction and capture to identify customers in real-time. Our solution has allowed various banks, insurance companies & businesses to experience the following benefits –

- Easy & quick onboarding without physical presence

- Reduced turnaround time for account opening

- Paper-free documentation

- Safe & remote onboarding for vulnerable customers

- Increased reach due to a presence-less & digital process

- Low-cost and efficient operations through digitization

We have helped our customers reduce onboarding costs by 90%, KYC drop-offs by 20%, and TAT by 99%.

Are you ready to onboard using video KYC? Book a demo with us now!