cKYC: A Primer

KYC is a fairly ubiquitous term in the regulated sector. Know Your Customer or KYC is a requirement for customers to avail the services of businesses in the BFSI sector and is in place to prevent cases of financial fraud including money laundering, illicit usage of funds, and the funding of criminal activities.

Since all organizations in the BFSI sector must abide by KYC norms, this would indicate that KYC is to be performed every single time a customer wants to avail the financial services from a bank, securities firm or insurer. This would be the case even if the customer has already completed KYC with another business.

It doesn’t take a lot of imagination to see that this repeated KYC compliance is a burden on both customers and businesses, especially since the customer’s KYC information would already be available.

cKYC was instituted precisely to alleviate this burden of multiple KYC transactions.

What is cKYC?

Central KYC (cKYC) is a directive of the Indian Ministry of Finance, first announced in the Union Budget of 2012-13, and subsequently functional from 2016.

This directive aims to remove the redundancies in the KYC compliance process by creating a single database where all the KYC information of customers is verified and then stored. This database is called the Central KYC Records Registry (CKYCR).

CKYCR is managed by the Central Registry of Securitisation, Asset Reconstruction and Security Interest of India (CERSAI).

CERSAI functions differently from other KYC Registration Agencies (KRAs), in that it’s a comprehensive database that verifies and stores customer KYC information, and doesn’t store in-person verified KYC information on individual systems.

How does cKYC work?

cKYC needs to be completed just once to avail the financial services. Upon completion of cKYC after the submission & verification of the required documents, the customer will receive a 14-digit KYC Identification Number (KIN) via SMS on their registered mobile number and via email.

The customer can then use KIN to complete KYC with any other bank, insurer, NBFC, or securities intermediary without submitting KYC documents all over again.

Businesses can simply use the KIN to retrieve the customer’s verified cKYC stored with CERSAI and complete KYC verification.

This process streamlines the KYC verification procedure and makes it simpler for everyone involved.

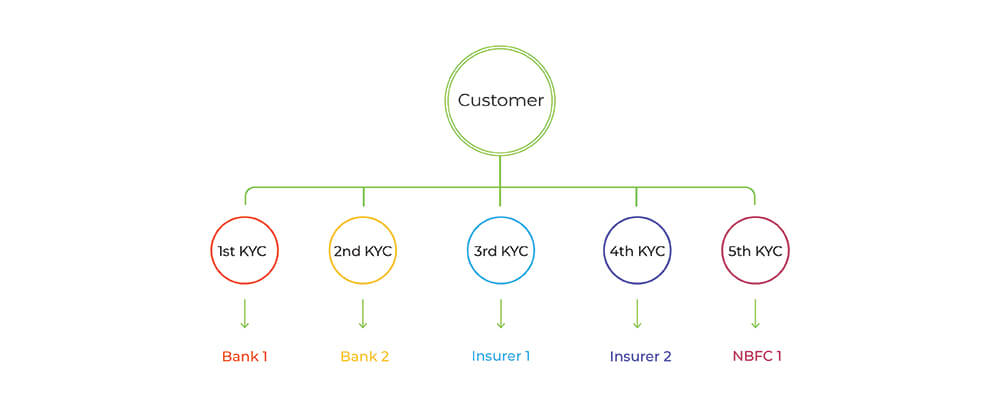

Here’s what KYC verification was like before and after cKYC.

Before cKYC

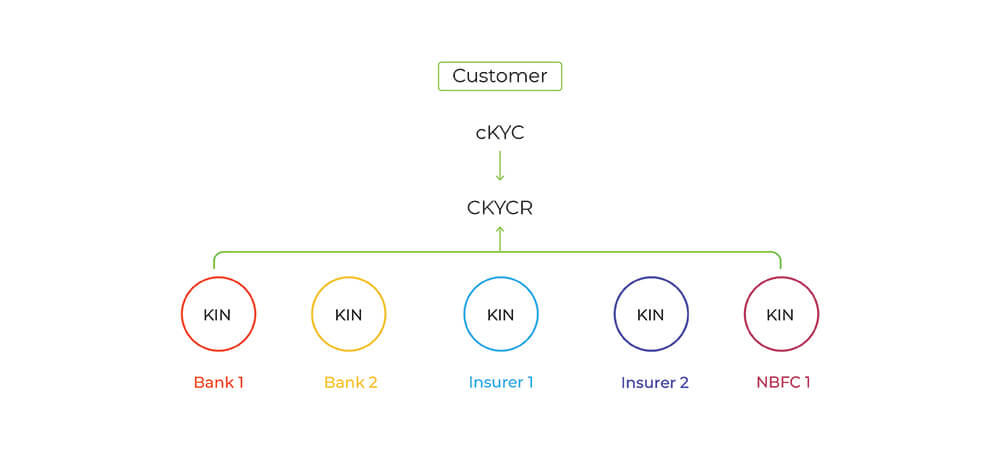

After cKYC

After cKYC

As evidenced above, cKYC does away with multiple KYC transactions by allowing financial service providers to verify a customer’s KYC using just their KIN.

How can you complete cKYC?

cKYC currently is a paper-based process and therefore involves the submission of documents & photos for completion.

Here are the documents required for cKYC.

- A filled & signed cKYC form

- A self-attested Proof of Identity

- A self-attested proof of Address

- A photograph

Once these are submitted to an FI, KRA, AMC, distributor or any registrar (such as CAMS), they’re sent to CERSAI who verifies them, and stores the KYC information.

Upon completion of cKYC, the customer will receive a 14-digit KIN within 2-5 working days. The status of investor cKYC can also be checked using the Karvy KYC check portal.

The documents required for cKYC can also be submitted by a Financial Institution (FI) using file transfer or through the bulk upload mechanism.

It’s important to note here that while PAN is not mandatory for the completion of cKYC, it is a requirement for availing financial services in the securities market, and therefore the submission of a self-attested copy of the PAN card is required for any investor to complete cKYC.

Additionally, NRIs looking to invest in the Indian securities market must also include a FATCA declaration in their cKYC application. This means that NRIs will have to disclose their foreign income to the tax authorities of the USA to complete cKYC.

cKYC details can also be updated using the same cKYC registration form, and the status of updation can be checked the same way.

Features of cKYC

cKYC was instituted to simplify and streamline the KYC process, and it does this in a number of ways.

Here are a few of the stand-out features that make cKYC an immensely useful tool for compliance.

- Every customer’s KYC information is linked to a unique identifier – either the KIN or the cKYC number linked with ID proof.

- Financial service providers can search and download KYC records with ease. FIs can use the bulk download option simply by entering the cKYC identifier and then access the KYC records after authentication.

- Once a customer’s KYC records have been updated on CKYCR, all the linked FIs will receive a notification regarding the update.

- Customers can link their KYC to multiple correspondence addresses.

- The cKYC data submitted to CERSAI will undergo a deduplication process based on the demographic and identifying details. KYC matches based on this process will then be submitted to FIs for resolution.

cKYC accounts also vary based on the documents submitted for cKYC verification. There are 4 types of cKYC accounts –

- Normal account: A normal cKYC account is created if the customer submits PAN, Aadhaar, Voter ID, Passport, Driving License or NREGA job card as proof of identity.

- Simplified measures account: This account is created when the customer submits any other Officially Valid Document (OVD) as proof of identity. Simplified measures accounts possess a cKYC identifier that’s prefixed with an ‘L’.

- Small account: This account is opened when a customer submits just their identifying details along with a photograph. The cKYC identifier for these accounts is prefixed with an ‘S’.

- OTP-based eKYC account: This sort of account is opened for a customer when they perform OTP-based eKYC for customer identification and also provide a photograph. The cKYC identifier in this case is prefixed with an ‘O’.

Finally, here are some additional details to note about cKYC.

- cKYC is currently only available for individuals, both nationals and NRIs.

- FIs are charged for accessing cKYC data from cKYCR. The charges for creating, downloading & updating a cKYC record are 0.80 INR, 1.10 INR & 1.15 INR respectively.

- cKYC requires the additional identifying detail of the customer’s mother’s name, as opposed to regular KYC which does not.

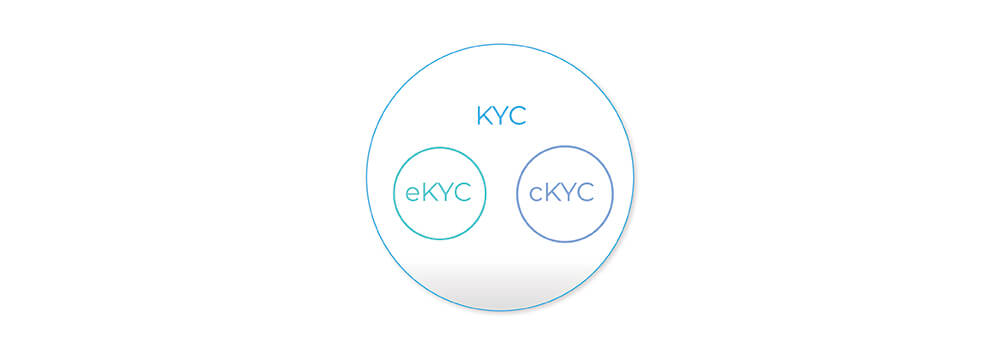

How is cKYC different from KYC & eKYC?

cKYC, KYC & eKYC are all terms that are seemingly related, there are differences between the three.

- eKYC is a digital customer verification procedure conducted for compliance with KYC norms. eKYC involves authenticating the customer’s KYC using the details available in the UIDAI database, after the customer validates the request via OTP, or offline via XML files or the QR code on the customer’s Aadhaar card.

- KYC is an umbrella term for the identification, due diligence and monitoring protocols put in place for FIs to prevent the occurrence of financial crimes. KYC has a large ambit which includes several paper-based, digital, & video-based procedures.

- cKYC, as mentioned before, is a provision to complete KYC just once. The main property of cKYC that sets it apart from eKYC and regular KYC is that the data resulting from the former is centralized, and the data resulting from the latter is stored by individual FIs or KRAs.

Benefits of cKYC

cKYC was introduced to ease the KYC process, and it has done so to an impressive extent.

Here are the key advantages of the cKYC process.

- Optimized costs for FIs

The financial burden of performing KYC is distributed across all FIs. By allowing for a centralized database of verified KYC information, just one FI will have to conduct a customer’s KYC and the rest will have access to the same if required. This optimizes the KYC costs for businesses across the BFSI sector.

- Reduced time taken for KYC verification

FIs and customers needn’t spend copious amounts of time conducting separate KYC verifications. cKYC massively reduces the turnaround time on KYC by centralizing the process.

- Unified KYC across BFSI

Verified KYC records are available sector-wide due to cKYC, allowing FIs to dedicate fewer resources to KYC verification and divert these resources into areas that will help them perform better.

- One customer, one KYC verification

cKYC massively boosts the customer convenience aspect of KYC, as a customer will have to get his or her KYC documents verified just once, and will no longer have to carry them around every time he or she requires financial services.

- Increased KYC usability

cKYC unifies KYC data across all financial regulators and boosts the efficiency of KYC verification by homogenizing KYC verification. With cKYC, a customer’s KYC needs to be verified just once to be used by any FI.

- Single updation

If a customer’s identifying details have changed, they only need to be updated once in the CKYCR, and not separately with every single FI associated with that customer. This is both cost-effective and extremely efficient.

Despite cKYC being a huge step in the right direction, there are still some kinks that need to be worked out and smoothed over.

What are the problems with cKYC?

cKYC suffers from a number of problems and pain points. Here are the most salient ones.

- The cKYC process is still paper-based. Customers must still provide paper-based documents and copies to FIs to complete cKYC.

- There is no structure in place to easily accommodate frequent cKYC record updation. While cKYC does include convenient provisions for KYC record updation, this process is also paper-based, i.e it involves filling up a form and submitting updated copies of KYC documents. This potentially results in bona fide challenges for accounts opened.

- Details cannot yet be shared between CERSAI & KRAs in case of investor KYC. There are currently no provisions in place for KRAs to share their KYC repositories with CERSAI.

- There are no automated bulk-upload options or data extraction features for FIs. FIs must still manually convert KYC documents and details into the bulk upload format and upload these to CKYCR. Additionally, FIs must also manually document the demographic and identifying information in these KYC documents.

- There are no options for FIs to perform a real-time search & download from CKYCR. FIs must lodge a request by using the requisite cKYC identifier and an authenticating factor to gain access to customer cKYC records. KYC data search can only be conducted once the information has already been downloaded by the FIs.

While these certainly are significant issues, the majority of these pain points can be solved by digitizing and automating the cKYC process.

How can cKYC be improved?

Digitization offers an easy and efficient solution to the problems of cKYC posed above. Here’s how.

- Digitize the cKYC process.

By allowing customers to upload scanned documents or document images, cKYC can be made even more hassle-free and efficient than it is now. FIs could use this to further reduce documentation costs, manual errors & TAT on cKYC.

- Use APIs for automated search and download.

By using an API to integrate the FI’s client data repository with the CERSAI application for search & download, FIs can easily find client data in real-time. The API could digitally encrypt the client data before sending it to the FI to ensure security.

- Utilize OCR-based data extraction methods for cKYC submission.

Once digital KYC documents have been submitted to the FI, OCR technology could be used to extract relevant details from these documents to submit to CERSAI for verification. This would reduce the TAT on cKYC verification.

- Employ an automated bulk upload option.

A bulk upload option would automatically upload client details to the cKYC application, after converting data into the bulk upload format. This would enable better user management, improve productivity and prevent data duplication.

These points are oddly reminiscent of another digital KYC process – Video-based KYC. But how can we use the model of Video KYC to improve cKYC?

Video KYC – A digital model for cKYC

Video KYC is the unofficial umbrella term for several video-based KYC verification processes that have recently been instituted by Indian regulators.

The first instance of Video KYC is RBI’s Video-based Customer Identification Process (V-CIP), which was closely followed by IRDAI with the Video-based Identification Process (VBIP), and then SEBI with the Video In-Person Verification Process (VIPV).

Video KYC essentially involves an FI digitally conducting KYC verification using a seamless, real-time & encrypted video-based process in which an official interacts with the customer over video. The main features of video KYC are –

-

- Image-based KYC data extraction

- Automated KYC document verification

- Questionnaire-based interaction between the customer and a trained official

- Facial matching & geo-tagging

So how can these techniques be used to optimize & expedite cKYC?

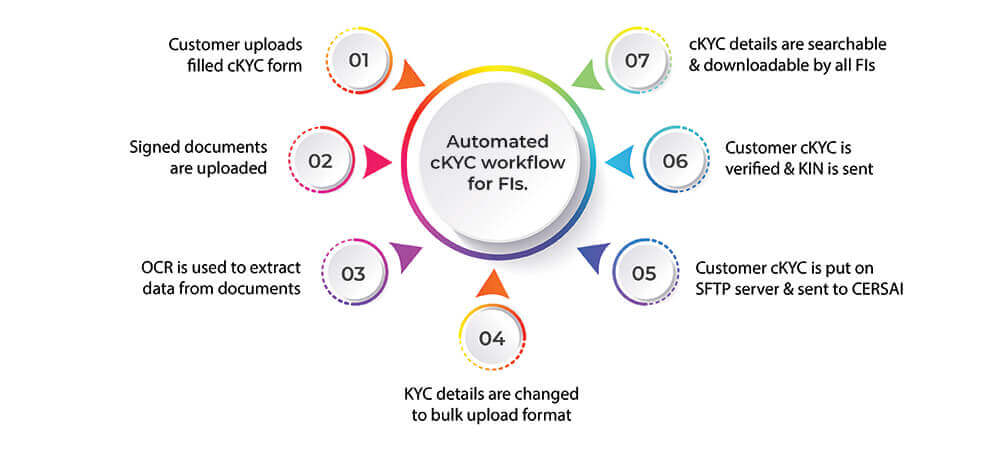

Here’s an automated cKYC workflow for FIs.

This digitized workflow optimizes expenses & time by leveraging data extraction techniques with existing cKYC norms.

The advantages of digitizing cKYC

Digitization of KYC verification affords numerous benefits to FIs and customers alike. Here are some of the advantages of digital cKYC.

- Reduced expenses.

Digitizing KYC verification entails massive financial benefits for FIs.

SignDesk’s clients have seen up to 90% reduction in operational expenses by employing digital KYC verification methods such as Video KYC.

- Shorter turnaround time.

Automating KYC verification has been shown to significantly reduce the turnaround time for customer KYC.

Reports indicate that digitizing KYC precipitates a 99% reduction in TAT, from days to within 10 minutes.

- Improved productivity & fewer manual errors.

Reducing paper-based documentation often massively improves worker productivity and reduces the manual errors that frequently occur during KYC verification.

According to studies, FIs can boost productivity by 80% by employing digital documentation methods.

- Improved security & fewer forgeries.

Automated KYC verification improves the security of the KYC process by ensuring client data security. Data extraction additionally reduces the chances of duplication & protects against forgeries by using ML-based anti-fraud methods.

- Paper-free documentation.

FIs spend too much time & money to keep their paper-based documentation functioning. Going paper-free helps businesses reduce costs, boost efficiency, reduce errors & generally improve returns on investment.

Digital cKYC, therefore, could prove to be a serious game-changer if implemented.

However, digital KYC verification can still greatly help FIs out by reducing costs & shortening TAT. So how can you perform KYC digitally?

How can you perform KYC digitally?

SignDesk is a trusted & award-winning KYC verification service provider, using AI-powered verification solutions to help businesses automate their documentation.

We use real-time document verification techniques, OCR-enabled image data extraction, facial matching & ML-based fraud filters to automate and expedite the KYC verification process.

Our verification solutions have helped our 250+ clients reduce onboarding expenses, cut down on KYC drop-offs, reduce TAT by 99%, and safeguard against fraud using cutting edge compliance technology.

Our efforts to automate KYC have been recognised in the form of numerous awards, the latest being the Best AI/ML Product at InnTech 2020, and the Global Banking & Finance Review’s Best Digital Onboarding Product of 2020.

Are you ready to join 50+ major banks and start onboarding with Video KYC? Book a demo with us now and let’s get started!